The Default Provider: America’s Reliance on Family Caregivers

How America outsources elder care to families, and who pays the price.

Somewhere in America at this very moment, a 52-year-old woman is catching up with insurance paperwork while her mother sleeps in the next room. She has rearranged her work schedule, used every available hour of time off, drawn down her savings, and stopped contributing to her 401(k). She has not had a vacation in three years and between work, caring for her mother and raising her children, she rarely gets any time to herself. She has had countless interactions with doctors and learned how to advocate for her mother’s care, but her own health has suffered. This woman is, statistically speaking, the American long-term care system.

There are an estimated 59 million family caregivers of adults in the United States, representing roughly one in four American adults, according to research from AARP and the National Alliance for Caregiving. (1) They provide care that the healthcare system does not, that the government largely will not fund, and that the market cannot profitably supply at the scale required.

“It’s past time for a national reckoning with how we value care in this country”

Among wealthy nations, America is a stark outlier. It spends less per capita on long-term care than nearly every comparable OECD country, while spending far more on healthcare overall. (2) The gap between what the government funds and what aging actually costs is filled by families. In an AARP analysis released last week, the economic value of unpaid family labor was estimated at more than $1 trillion in 2024. That amounts to more than all federal, state and local Medicaid spending in the same year ($931.7bn). (3) This is not a social safety net supplemented by family love, but a system of care built almost entirely on private sacrifice.

“It’s past time for a national reckoning with how we value care in this country - and for Congress, states, and employers to act with policies that reflect the essential role family caregivers play in our society,” says Jason Resendez, President and CEO of the National Alliance for Caregiving.

The Invisible Workforce

The archetype of the American caregiver is the eldest adult daughter in a multi-generational family. The average caregiver is 51 years old; three in five are women, and about a third are simultaneously raising children - what demographers call the “sandwich generation.” Among caregivers under 50, the proportion caught between the needs of their parents and their children rises to nearly half.

The tasks they perform have also expanded well beyond what the term “caregiving” implied a generation ago. Caregivers manage everything from basic daily care needs such as bathing, dressing, meals and mobility, to responsibilities that resemble those of nurses or case managers: managing medications, accompanying patients to appointments, keeping track of test results and translating medical instructions into daily routines. More than half of family caregivers now perform tasks like wound care, catheter maintenance, and post-surgical monitoring - clinical work that hospitals and insurers have offloaded onto families by discharging patients faster and leaving the rest to whoever is at home.

“Nobody prepared me for what this actually is. I am a full-time nurse, social worker, insurance negotiator and emotional support system, and I am doing all of it alone.”

The average caregiver devotes roughly 25 hours a week to these duties; a quarter devote more than 40 hours. This is equivalent to a full-time job performed without pay, benefits, or legal protection, often putting caregivers under tremendous financial strain. By some estimates, women spend up to 50 per cent more time on caregiving tasks than their male counterparts, and the average duration of a caregiving stint is 5.5 years. (4)

Costs for Caregivers and the Economy

Caregiving has a dangerous compounding effect for women’s financial future in particular. A MetLife analysis found that working women who serve as caregivers lose more than $320,000 over their lifetimes in wages, pension benefits, and Social Security accrual as a direct result of workforce exits, reduced hours, and forgone promotions. (5) One 2024 study found that caregivers risk a 90 per cent reduction in retirement savings compared to non-caregivers. (6) Women, who are overrepresented as caregivers and who statistically live longer, enter old age with less and then face longer periods of needing care themselves.

Race amplifies every dimension of this. Black and Hispanic families are more likely to provide informal care and less likely to have access to paid alternatives. They are more likely to live in areas with fewer home care agencies, fewer geriatric specialists, and longer waiting lists for Medicaid-funded home and community-based services. The sandwich generation burden falls disproportionately here too: Latino and Black caregivers under 50 are among the most likely to be caught between the needs of aging parents and young children.

The physical and psychological toll of sustained caregiving is equally clear. Nearly three-quarters of caregivers report significant stress, and caregivers over 65 are markedly more likely than their peers to carry multiple chronic conditions. And yet nearly half of all caregivers receive no support of any kind — no respite care, no counseling, no financial assistance, and no formal training for the clinical tasks they are asked to perform. (7)

For Jennifer, a California woman who left her job and moved to Massachusetts when her mother’s fall was followed by a cancer diagnosis, the hardest part is not the work itself. “Nobody prepared me for what this actually is. I am a full-time nurse, social worker, insurance negotiator and emotional support system, and I am doing all of it alone, three thousand miles from my own life. I love my mother, but I also feel like I have disappeared.”

American employers absorb a portion of these costs without always recognizing them. A Harvard Business School study found that nearly a third of American workers have left a job due to caregiving responsibilities. The costs to employers, through turnover, lost institutional knowledge, and reduced productivity, are substantial but largely invisible because most companies don’t measure them. (8) Employer response has been slow and uneven: only 27 per cent of private-sector workers had access to any paid family leave as of 2023, and it remains largely a privilege of higher-income workers.(9) The federal Family and Medical Leave Act guarantees 12 weeks of unpaid, job protected leave, but less than 60 per cent of workers are actually eligible — and those who need it most, including low-wage and part-time workers, are the least likely to qualify or to be able to afford unpaid leave.” (10)

The Policy Gap

To understand why American families bear so much of this burden, it helps to understand the current structure of public support. The United States has Medicare, which covers acute care but almost nothing in the way of long-term support. Medicaid covers long-term care, but only after a recipient has spent down their assets to near-poverty level. Private long-term care options are prohibitively expensive for most families. A year in a nursing home now costs more than $110,000 at the national median, while home health aide services cost between $33 and $35 an hour in most markets and are chronically short-staffed. (11) Between these two extremes lies what researchers have called the “forgotten middle”: middle-class families caring for aging relatives with no public support and no realistic way to afford private alternatives. (12) Long-term care insurance, once a viable private-market alternative, has contracted sharply as insurers have exited the market after years of mis-priced premiums.

The federal program most directly aimed at this gap - the National Family Caregiver Support Program, established in 2000 - has seen its budget grow from $150 million at inception to roughly $200 million in 2024, barely keeping pace with inflation while the population it serves has expanded by tens of millions. The program’s future is now in further doubt after the Trump administration’s restructuring of the Department of Health and Human Services in 2025.

“The political inertia reflects a longstanding, though largely silent consensus that families will provide.”

There have been other genuine, if modest, advances. The 2018 RAISE Family Caregivers Act required the federal government, for the first time, to develop a national strategy to support caregivers, a document that was finally released in 2022. In 2024, Medicare introduced a billing code to reimburse physicians for training and educating family caregivers, a small but meaningful acknowledgment that caregivers are participants in the healthcare system. At the state level, Oklahoma, Nebraska Georgia, Missouri, New Jersey, North Dakota, and South Carolina have all introduced caregiver tax credits since 2023. Fourteen states and the District of Columbia now have paid family leave programs, though their scope varies considerably and most cover only short-duration leaves. Washington State has launched an ambitious universal long-term care insurance fund and seven states are considering similar programs.

The larger federal picture is moving in the opposite direction, however. The most consequential caregiving-related federal action in 2025 was nearly $1 trillion of cuts to Medicaid over ten years, threatening access to home and community-based services for millions of older Americans. A bipartisan bill to create a national catastrophic long-term care insurance program was reintroduced in 2025, but it faces a political environment hostile to new social spending.

The political inertia reflects a longstanding belief that families will provide. This assumption has proven durable precisely because the labor it relies on is invisible: performed in private homes, uncounted in GDP, and not concentrated in a swing district. Public opinion surveys consistently show that roughly 80 per cent of both Republicans and Democrats believe the government should do more to support family caregivers, (13, 14) but the consensus has yet to find legislative expression.

A Daunting Future

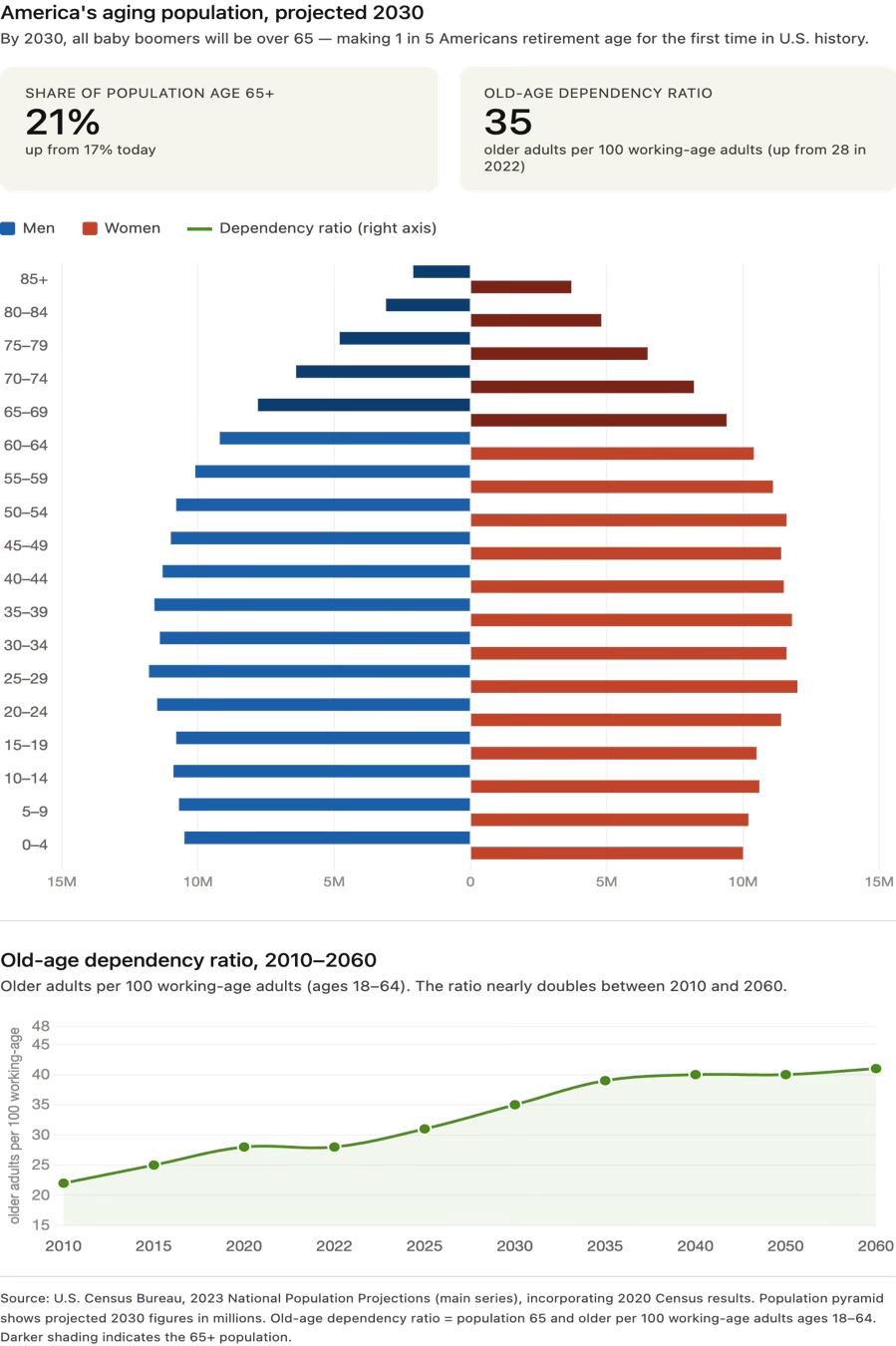

The demographic arithmetic is unforgiving. All 73 million Baby Boomers will have passed age 65 by 2030. By that year, Americans over 65 will outnumber children under 18 for the first time in the country’s history. The number of adults who are simultaneously working and providing care has already risen from one in seven in 2020 to one in five today. That ratio will worsen in line with the old-age dependency ratio: the number of older adults per 100 working-age adults (see graph).

More troubling still is the supply side. The informal caregiver pool is thinning. Smaller family sizes, higher rates of childlessness among Millennials and Generation Z, and the geographic dispersal of families mean that the next cohort of older Americans will have fewer potential family caregivers per person than any previous generation. The paid home-care workforce, the most plausible substitute, is itself chronically understaffed, plagued by poverty wages, high turnover, and a looming shortage as the sector tries to absorb demand that will roughly double by 2050. The country is arriving at a demographic inflection point with its care infrastructure substantially unprepared.

The United States has built its long-term care system on an assumption that someone at home will handle it. For millions of Americans, that assumption is a job description they never applied for.

In next week’s Aging Almanac, we’ll examine why that job so often falls to a single family member, and what families can do to share the load.

That is SO well written!

And quite frightening…

Great data Saskia… sobering and honest